The European Central Bank is set to keep borrowing costs on hold for a third meeting while

stepping up efforts to convince investors that interest-rate cuts aren’t imminent. The deposit rate will be

left at 4%, according to all economists polled by Bloomberg. How long it stays there, though, is an everhotter topic, with President Christine

Lagarde joining many of her colleagues in

signaling a summer reduction is “likely.”

Christine Lagarde takes on traders when she

speaks after today’s policy decision. Though

the ECB is universally expected to leave rates

unchanged, Lagarde may use her press conference to again push back against market

expectations of a first cut in April.

The next UK government will inherit the most challenging set of tax and spending problems in 70 years,

the Institute for Fiscal Studies said.

Soaring debt and rising interest rates have added about £50 billion a year to government borrowing

costs, stripping public services of much-needed funding and driving the UK tax burden to a postwar

high.

The government will need to raise more tax than it spends on everything other than debt interest from

now onwards, the think tank said. The last time the UK ran a primary surplus was in 2002.

China made another decisive move to address its ongoing economic woes, this time

by saying it will cut the reserve requirement

ratio for banks within two weeks while hinting at more support measures to come. The

RRR will be lowered by 0.5 percentage

points on Feb. 5 to provide 1 trillion yuan

($139 billion) in long-term liquidity to the

market. China’s $6 trillion stock rout reveals a painful truth for Xi Jinping: people are hopelessly gloomy

about the economy, and that pessimism is becoming increasingly hard to ignore at a time where everything—from the property bust, demographic drag and debt buildup—seem to be going wrong all at

once.

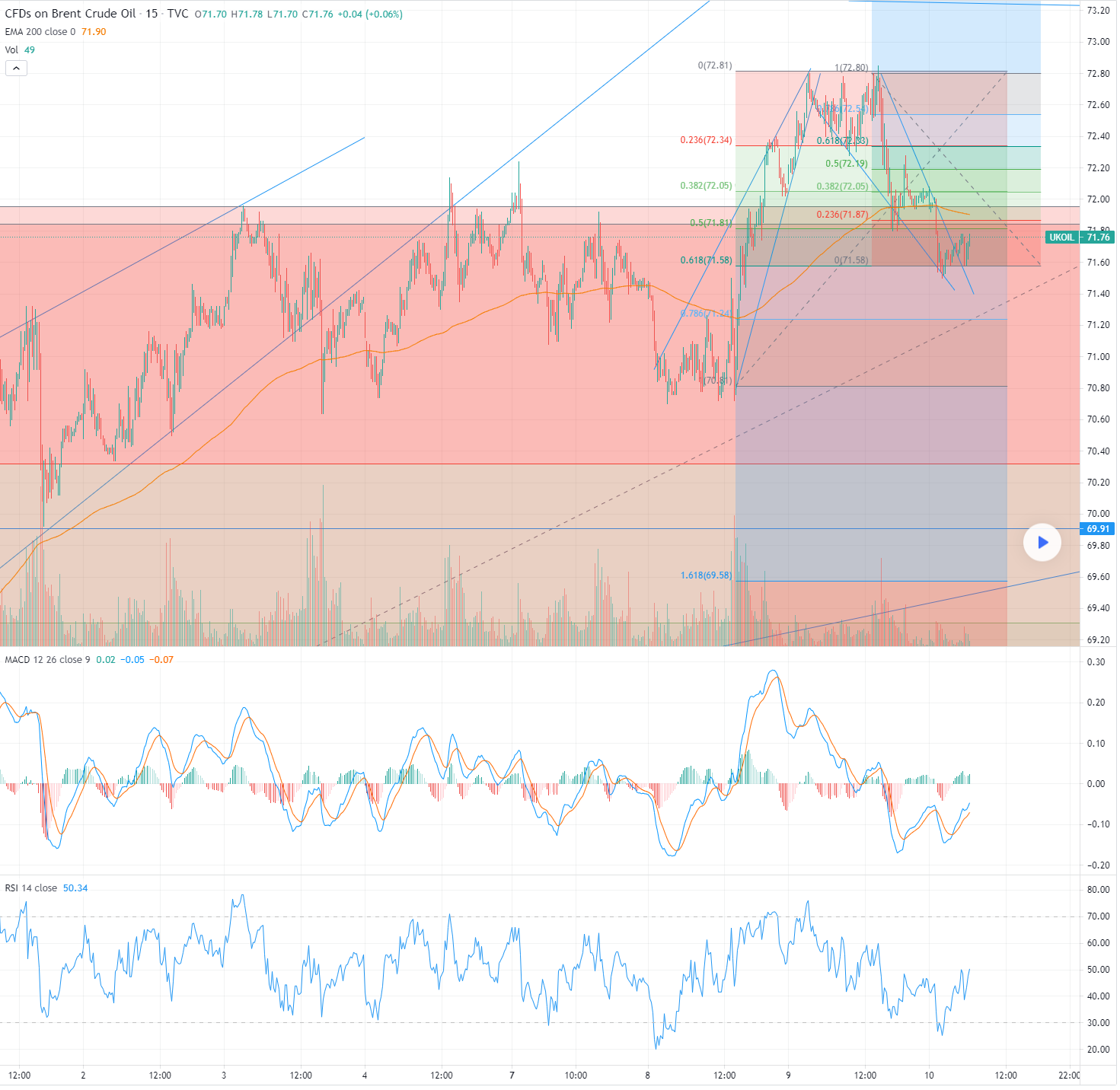

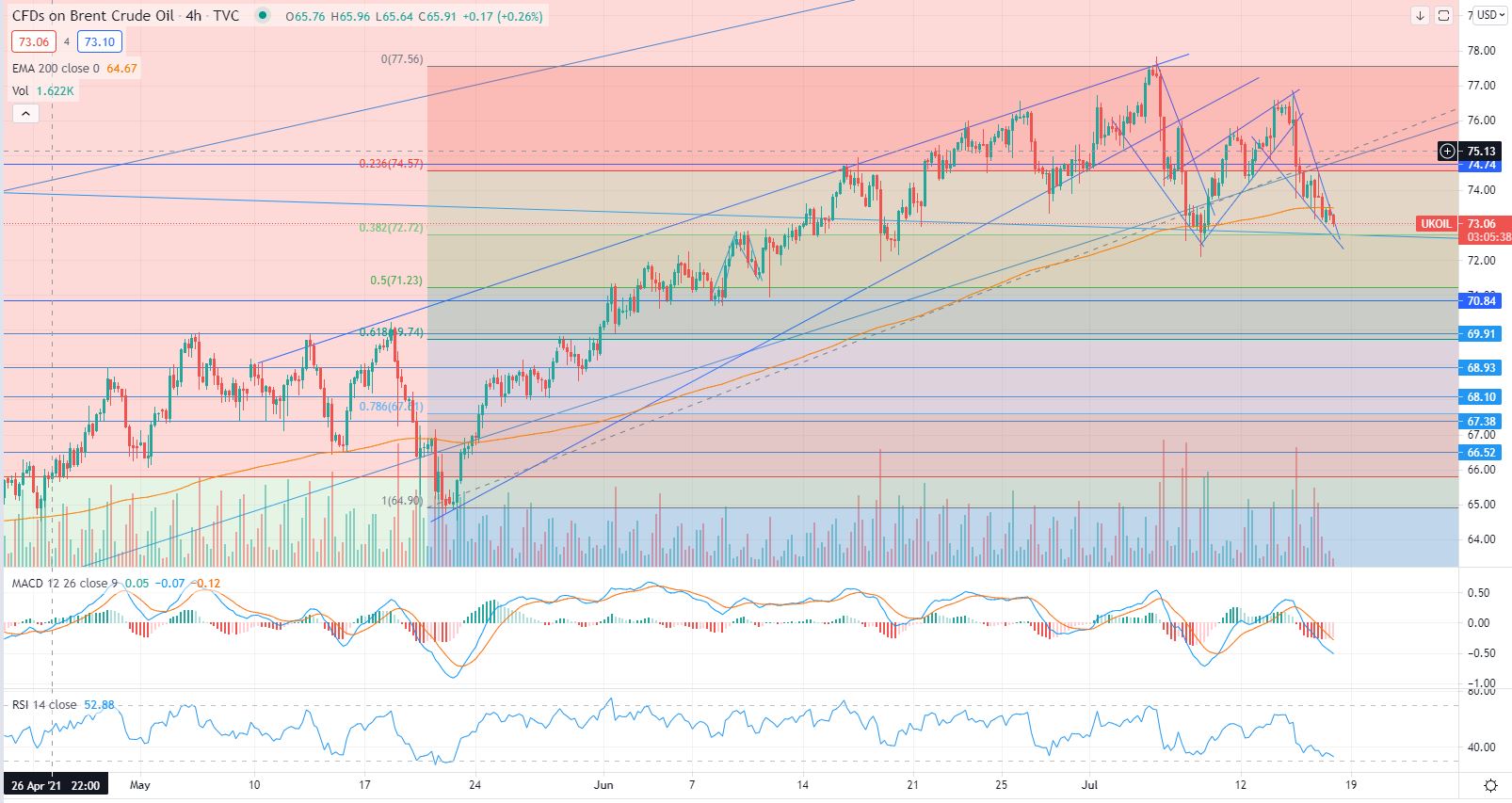

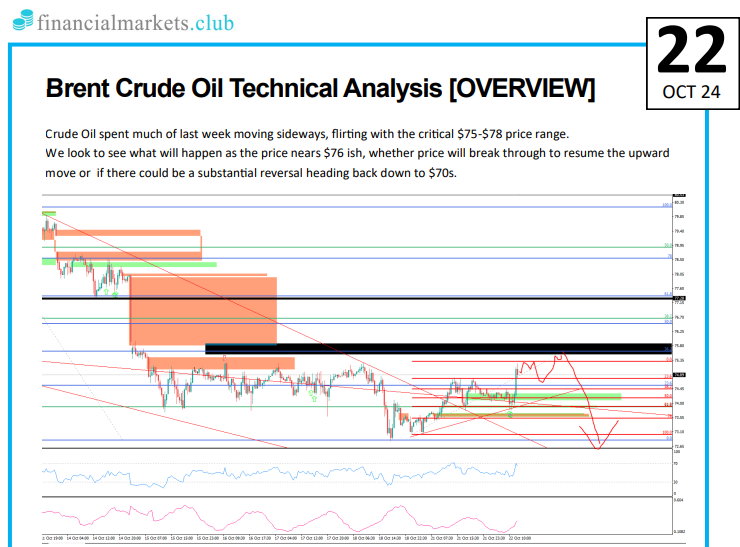

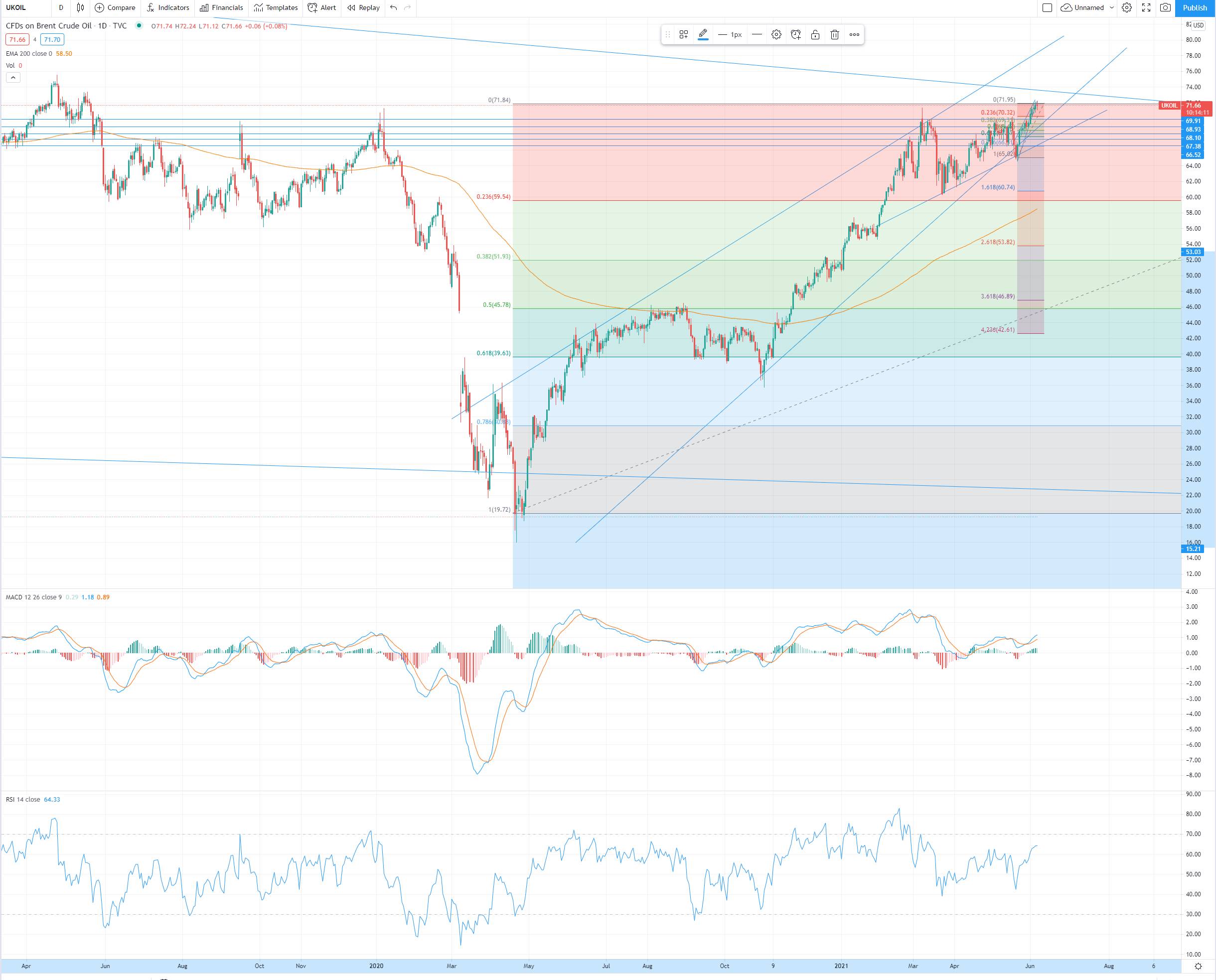

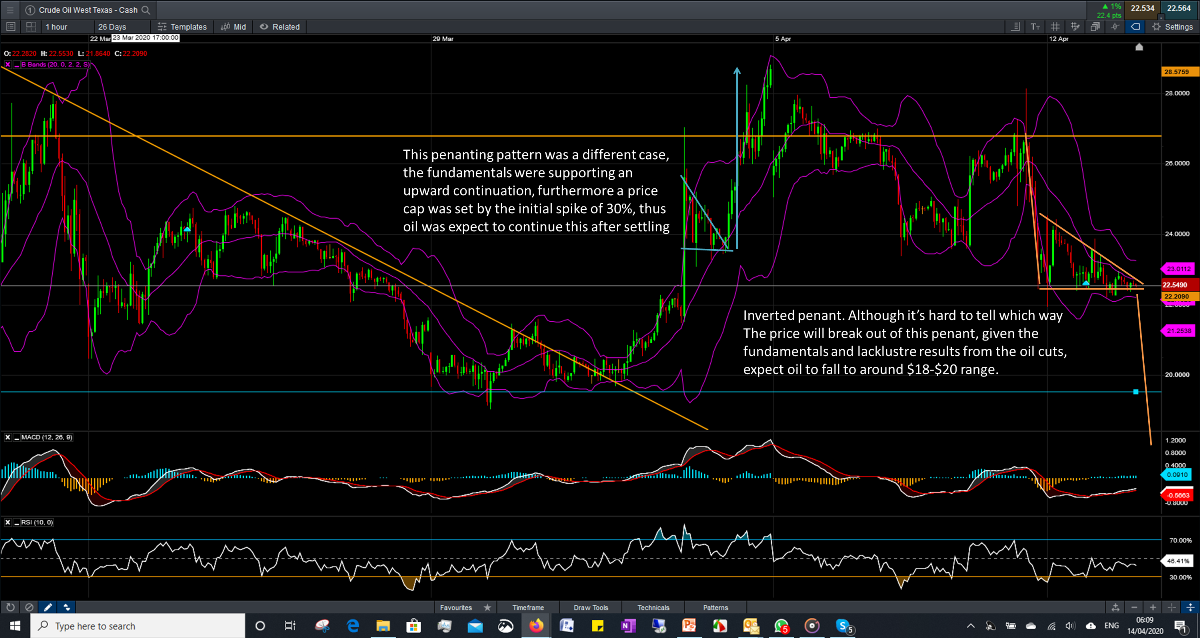

U.S. WTI crude oil futures settle at $75.09 per barrel, rising $0.72 or 0.97% while Brent Crude futures

settle at $80.04 per barrel, +0.49 or 0.62%, getting a

boost from a bigger-than-expected U.S. crude storage withdrawal, Chinese economic stimulus and geopolitical tensions countered concerns over tepid

demand.

The weekly EIA data showed a bigger-than-expected

9.2 million barrels of crude from stockpiles during

the week ended Jan. 19th.

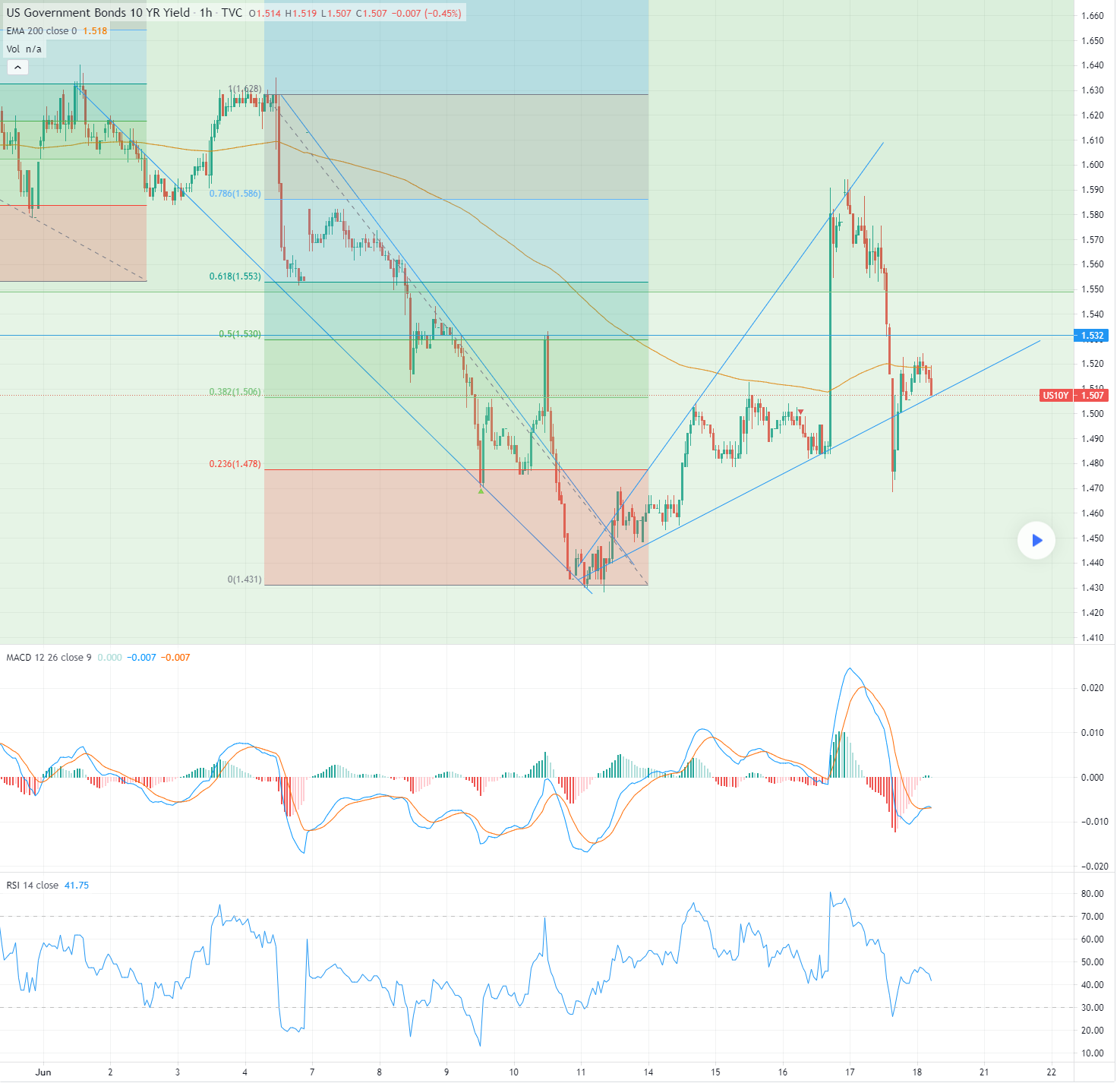

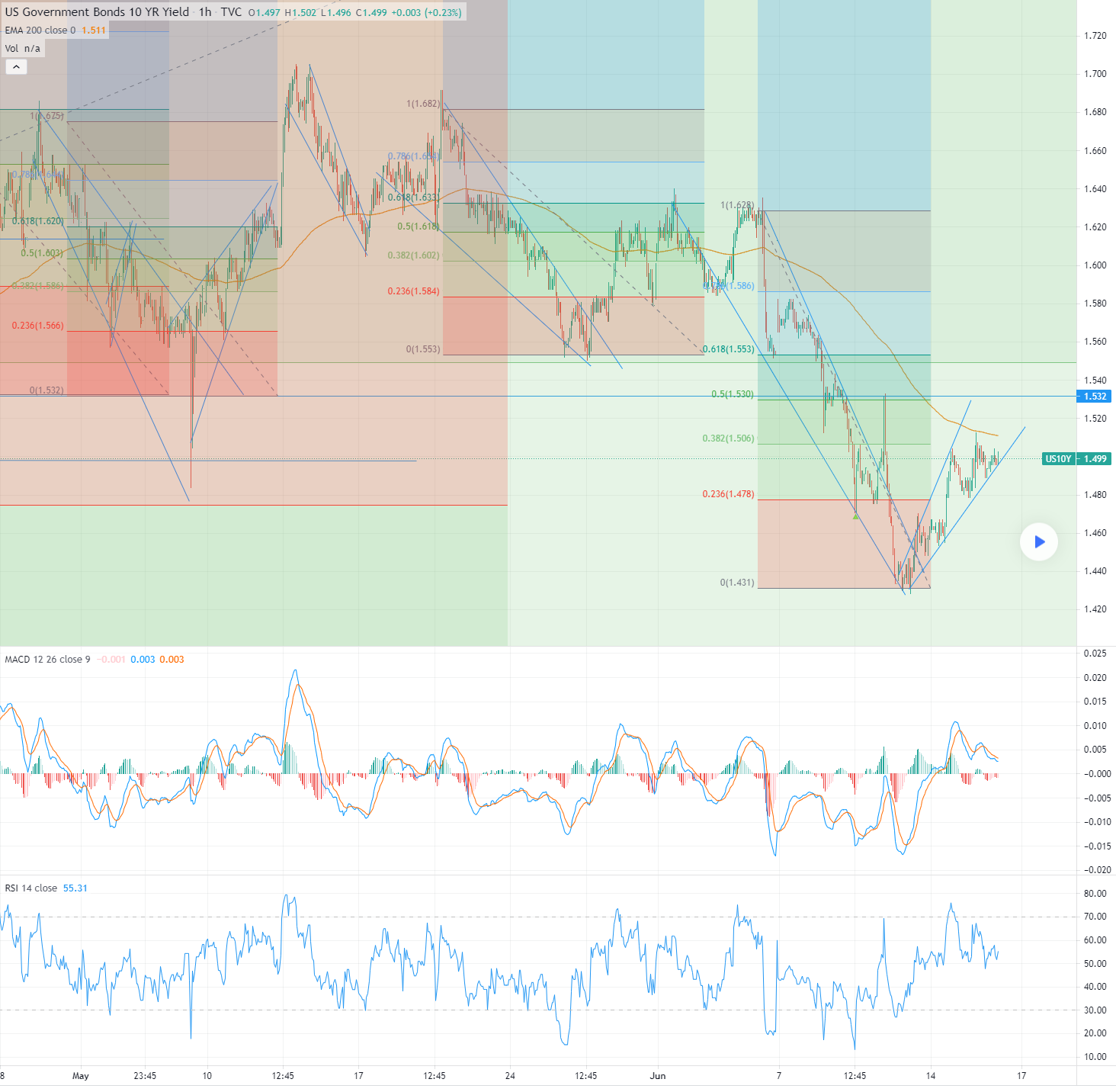

Treasury yields jumped across the board following a

weaker 5-year auction midday (10-yr above 4.17%,

30-yr above 4.4% for highest since early Dec and 2-

yr 10-bps move off lows). The US Treasury sold $61B

in 5-yr notes at a yield of 4.055% (2 bps tail) vs.

4.035% when issued prior, the biggest tail since Sept

2022 as the bid-to-cover ratio 2.31 (vs. 2.5 prior auction) and primary dealers take 20.37% of U.S. 5-year

notes sale, direct 18.69% and indirect 60.94%.

Treasury yields moved higher following the weaker

auction. Yields had already bounced off lows earlier

after better data when thew January flash manufacturing PMI was 50.3, up from December's 48.2 and

consensus of 47.2 and flash services PMI was 52.9,

up from December's 51.3.

The U.S. dollar also rose after the PMI numbers, but

the Dollar Index (DXY) remained in negative territory, falling 0.45%, with sharp declines vs. major rivals.

The euro posted its biggest move in a month, back

above the 1.09 level. The weaker 5-yr bond auction

added to the bounce in the dollar (which had hit 7-

week highs on Tuesday). Bitcoin prices rebounded

about 2% back to $40K but remains around 20%

from its January highs.next week.

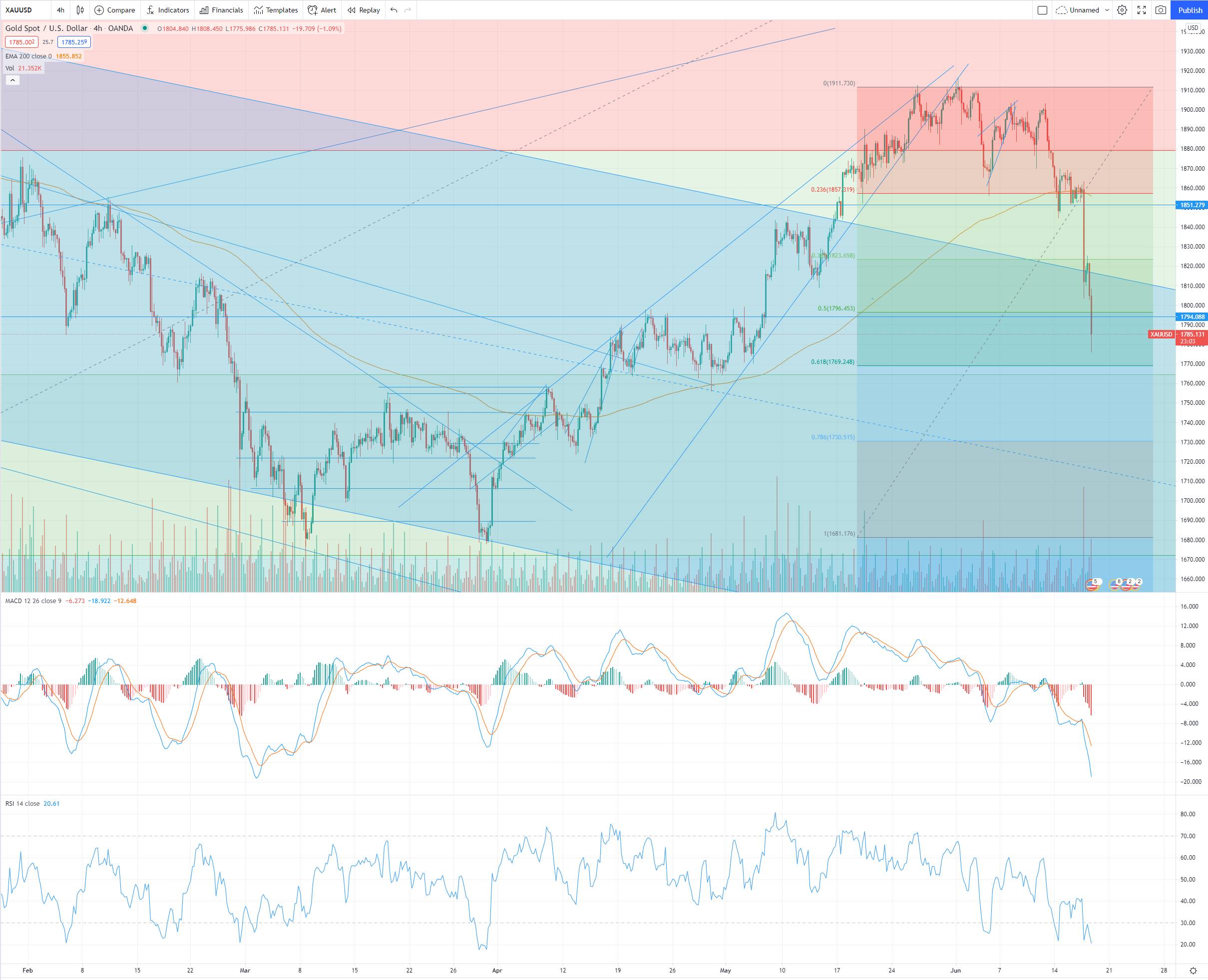

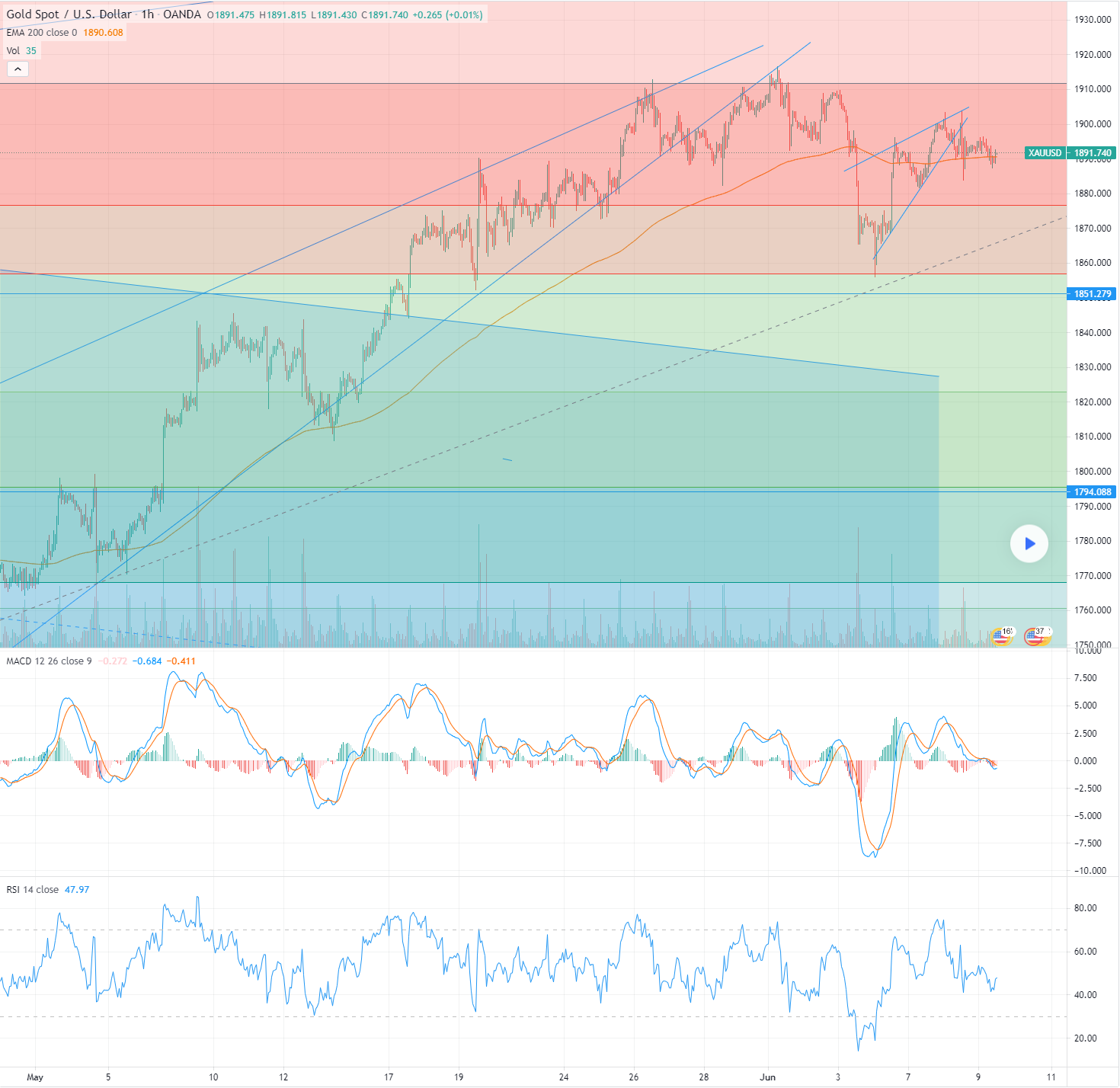

Gold prices fell -$9.80 to settle at $2,016 an ounce,

falling after a bounce in yields and as the dollar

pared losses.

Market Summary

FinancialMarkets

FinancialMarkets

Comments